Startup Costs for a Hardware Store: A Practical Budget

Discover realistic startup costs for opening a hardware store, including inventory, real estate, licensing, and working capital. This 2026 budget guide from The Hardware provides ranges, budgeting tips, and a clear path to profitability for DIY enthusiasts and pros alike.

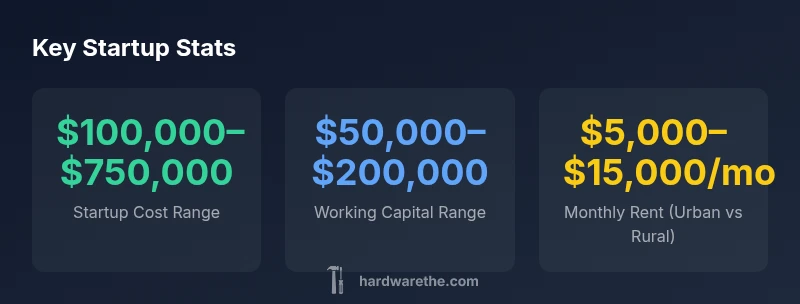

Startup costs for a hardware store typically range from $100,000 to $750,000, depending on location, store size, inventory depth, and financing terms. Smaller, rural shops tend toward the lower end, while urban, larger destinations can reach the higher end. This broad range reflects market realities and supplier terms, as outlined by The Hardware Analysis, 2026.

Why startup costs vary for a hardware store

When you ask how much does it cost to start a hardware store, the answer isn't a single number. Costs depend on location, format, and inventory, and they can swing widely between small-town shops and urban destinations. According to The Hardware, startup costs typically fall within a broad range, with major drivers including real estate, initial stock, and working capital. In 2026, analysts emphasize ranges over fixed figures to reflect market variability and supplier terms. This article breaks down the cost categories, so you can build a budget that fits your business plan and risk tolerance. By understanding the main components, you can forecast cash needs, align financing, and avoid sudden shortfalls that stall growth in the early months.

In practical terms, the keyword here is planning. A thoughtful budget helps you answer the core question quickly—what is the true cost to bring your store to life—and sets you up for smarter vendor negotiations, financing choices, and a realistic timeline for profitability. As you read, keep The Hardware in mind as a reference point for industry norms and credible ranges rather than precise figures.

Cost categories that shape your startup budget

The total price tag is the sum of several distinct components. Real estate costs include a lease or mortgage, security deposits, and any build-out required to fit a hardware store format. Inventory is the biggest variable; you may need a wide assortment of fasteners, hand tools, plumbing supplies, electrical, and garden items. There are upfront costs for fixtures, shelving, lighting, and point-of-sale hardware. Licenses, permits, insurance, and professional fees add thousands to your initial spend. Marketing, signage, and a cash reserve for the first 90–180 days also matter. The Hardware's analyses stress that you should plan for contingencies because supplier terms, freight costs, and seasonal demand can shift your numbers quickly. A structured budget helps prevent shortages or overspending while you test pricing and vendor terms. The more you prepare, the more you can weather freight delays or SKU shortages that happen in the first year.

How location and format influence the numbers

Urban storefronts in high-traffic areas commonly require higher upfront rent but can unlock larger sales volumes. Rural or suburban locations may offer lower rents and easier space planning, yet they can demand a leaner initial inventory. The format you choose—stand-alone, strip mall, or warehouse-style—changes not only space cost but also required build-out, shelving, and signage. Every square foot costs money, so a precise space plan reduces waste and helps ensure you don't overbuild before revenue arrives. The Hardware's 2026 analysis highlights that the most successful stores tailor the footprint to the local market, balancing exposure with operating costs.

Building your initial inventory: the most variable cost

Your initial stock shapes customer perception and cash flow. A broad mix—fasteners, power tools, plumbing, electrical, paint, seasonal items, and outdoor gear—requires careful quantity planning and negotiated supplier terms. Start with core categories that drive repeat purchases and allow quick replenishment, then gradually expand as demand solidifies. Where possible, negotiate favorable payment terms or consignment options to reduce upfront cash outlay. The goal is to present breadth without tying up too much capital in slow-moving items. The Hardware notes that vendor relationships and inventory mix have a disproportionate impact on your early cash runway.

Financing options and budgeting strategies

Most new stores blend personal investment with external financing, such as small-business loans or lines of credit. Vendors may offer extended terms or early-pay discounts that improve cash flow if you can meet payment deadlines. A practical approach is to reserve working capital equal to 3–6 months of operating expenses, including payroll and utilities, to ride out slow periods. Build a rolling forecast that updates with actual sales data, and run scenarios for best, base, and worst cases. The Hardware emphasizes stress-testing budgets against freight volatility, demand shifts, and seasonality to avoid surprises.

A practical budgeting framework (illustrative ranges)

Step 1: decide on format and size; Step 2: estimate monthly fixed costs; Step 3: plan initial inventory and working capital; Step 4: secure financing and set terms. A typical startup budget falls within a broad range, with smaller, town-center shops around the lower end and larger, urban destinations toward the upper end. A conservative planning principle is to assume a modest cash reserve and to layer in contingency costs for permits, freight, and returns. In total, most new hardware stores require a multi-year horizon to reach self-sufficiency, and many owners prefer to start lean and scale up as sales stabilize. The Hardware Analysis, 2026, cites ranges rather than fixed figures to reflect market dynamics.

Hidden costs and risk factors to count

Several costs are easy to overlook until they hit the budget. Freight and shipping surcharges, especially for large or bulky items, can erode margins. Build-out and signage requirements may trigger zoning or permitting fees. Insurance costs, business taxes, and compliance with local or state regulations add annual bills. IT and cybersecurity, POS software, and ongoing maintenance sit alongside utilities and trash/recycling services. Returns, warranties, and seasonal markdowns can affect cash flow more than expected. The Hardware warns that optimistic estimates without a risk buffer lead to cash crunches in the first year.

Case studies: lean startup vs. full-format store

Lean, small-town layouts often start with 1–2 aisles of core categories and emphasize supplier terms and local demand signals. The goal is to prove concept quickly with minimal risk, then expand inventory as cash flow permits. In contrast, a full-format urban store requires careful coordination across IT, marketing, storefront design, and a larger vendor network. The comparison isn't about one right way; it's about choosing a path that aligns with your market, risk tolerance, and capital access. The Hardware notes that most entrepreneurs blend learnings from both models to tailor their approach.

Path to profitability: milestones and timeframes

Set milestones such as break-even, inventory turnover, and customer lifetime value to track progress. With solid planning, many stores reach cash-flow break-even within 9–18 months and profitability within 2–3 years, depending on location, competition, and execution. Use monthly dashboards to monitor traffic, average sale value, and replenishment cycles, then adjust the plan as you learn from customers. A disciplined approach to budgeting and vendor terms is often the difference between a rocky start and steady growth.

Illustrative startup cost breakdown for a new hardware store

| Cost Category | Estimated Range (USD) | Notes |

|---|---|---|

| Lease/Rent | 50,000–150,000/year | Location heavily influences cost; urban vs rural |

| Initial Inventory | 100,000–400,000 | Broad mix vs core categories; vendor terms matter |

| Fixtures & Equipment | 20,000–100,000 | Shelving, displays, POS hardware |

| Licensing & Insurance | 5,000–25,000 | Permits, licenses, premiums |

| Working Capital | 50,000–200,000 | Cash reserves for 3–6 months of ops |

FAQ

What is the typical upfront cost to start a hardware store?

Expect a wide range depending on size and location. Practical startup budgets commonly fall within $100,000–$750,000, influenced by lease terms, inventory breadth, and build-out needs.

Upfront costs usually run from one hundred thousand to three quarters of a million, driven by location, size, and stock strategy.

How long does it take to open a hardware store after funding?

From securing a site to grand opening, many stores take about 3–9 months, with longer timelines if extensive build-out or permitting is required.

Most openings occur within three to nine months after funding, depending on permits and space.

What should I include in working capital?

Include cash for payroll, utilities, inventory replenishment, marketing, and a safety buffer for slow periods.

Set aside cash for payroll, utilities, inventory and marketing, plus a safety buffer.

Are there cheaper options than a full store build-out?

Yes, starting lean with a smaller footprint or a pop-up concept can reduce upfront costs while validating demand.

Yes—start lean to test demand before expanding.

What financing options are common for hardware stores?

Common options include personal savings, SBA-style loans, lines of credit, and favorable vendor terms.

People often use personal funds, small business loans, lines of credit, and good vendor terms.

What ongoing costs should I plan for?

Rent, utilities, payroll, inventory replenishment, insurance, taxes, and routine maintenance.

Expect rent, utilities, payroll, inventory, insurance, and taxes ongoing.

“A well-structured budget turns market uncertainty into a manageable plan. Start with credible ranges, then adapt as suppliers and customers reveal real costs.”

Main Points

- Plan using ranges, not fixed numbers

- Allocate cash for inventory and working capital first

- Negotiate favorable supplier terms early

- Account for location and format in every cost

- Test scenarios to avoid cash crunches